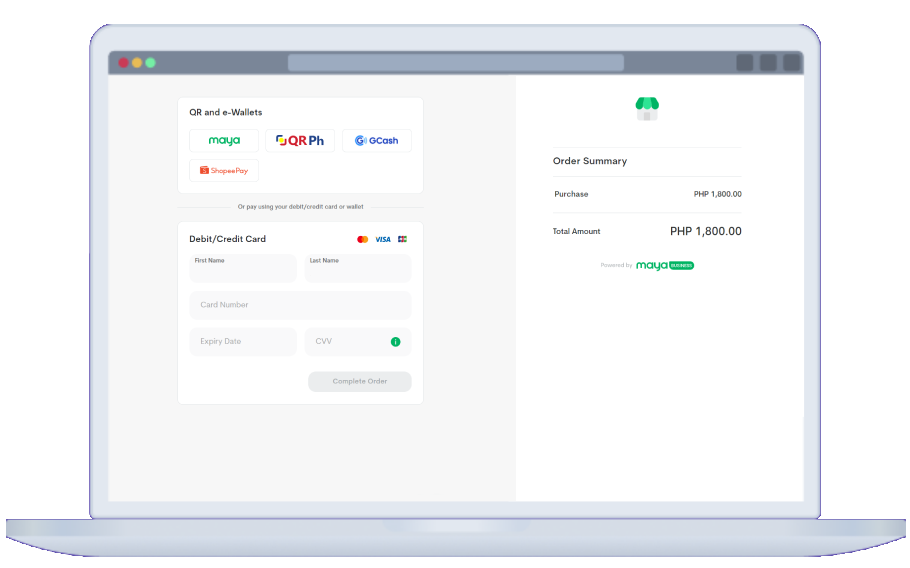

Let your customers pay online, in store, or through email, chat, a website, or an app

.png)

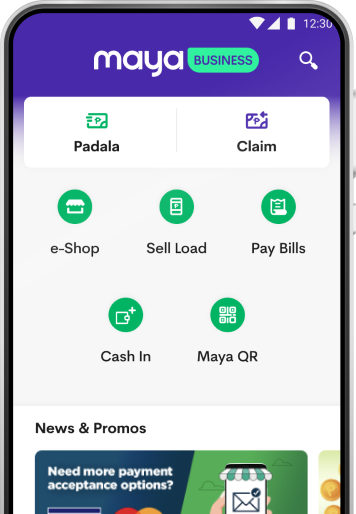

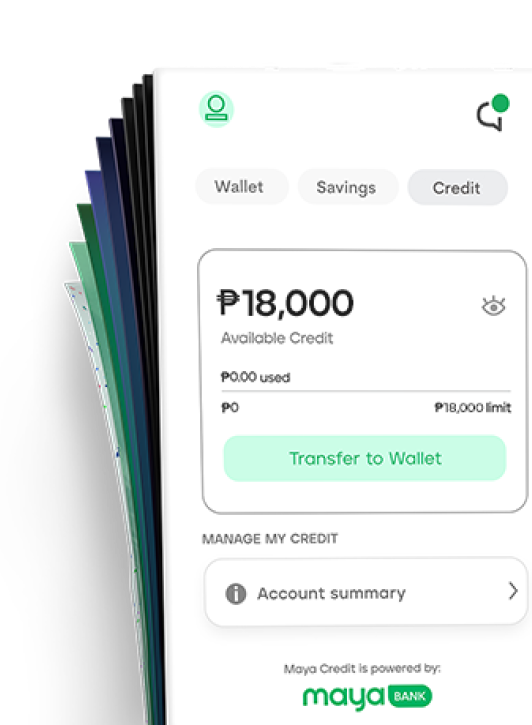

Your all-in-one business growth partner just keeps getting better

Starting July 14, 2024, Maya will be collecting withholding tax for each transaction for qualified merchants in compliance to BIR Revenue Regulations (RR) No. 16-2023 and Revenue Memorandum Circular (RMC) No.55-2024.

Tell me more

Make getting paid easier with your one-stop payment gateway

Take QR Ph and card payments with just one device

Enjoy easier money management and better security

Process and release payroll payments, allowances, and incentives efficiently

.png)

.png)

.png)